The Shadow Reckoning: Private Credit, Shadow Banking, and the Trigger for The Big Turning

How redemption lockdowns, zombie companies, and the maturity wall of 2026 expose the fault line that could trigger the reversal of the 80-year post-war debt super-cycle

In “The Big Turning: The Terminal Phase of the Debt Super-Cycle (2019-2026)” we traced the convergence of forces signaling the reversal of the 80-year post-war debt super-cycle. Sovereign debt at 122% of GDP. Interest costs consuming 19% of federal revenue. Gold overtaking US Treasuries in central bank reserves for the first time since 1996. Kinetic enforcement of the dollar in Venezuela and Iran. AI hollowing out white-collar labor. Public trust at 17%. Everything, everywhere, all at once.

That article ended with a question: what breaks first?

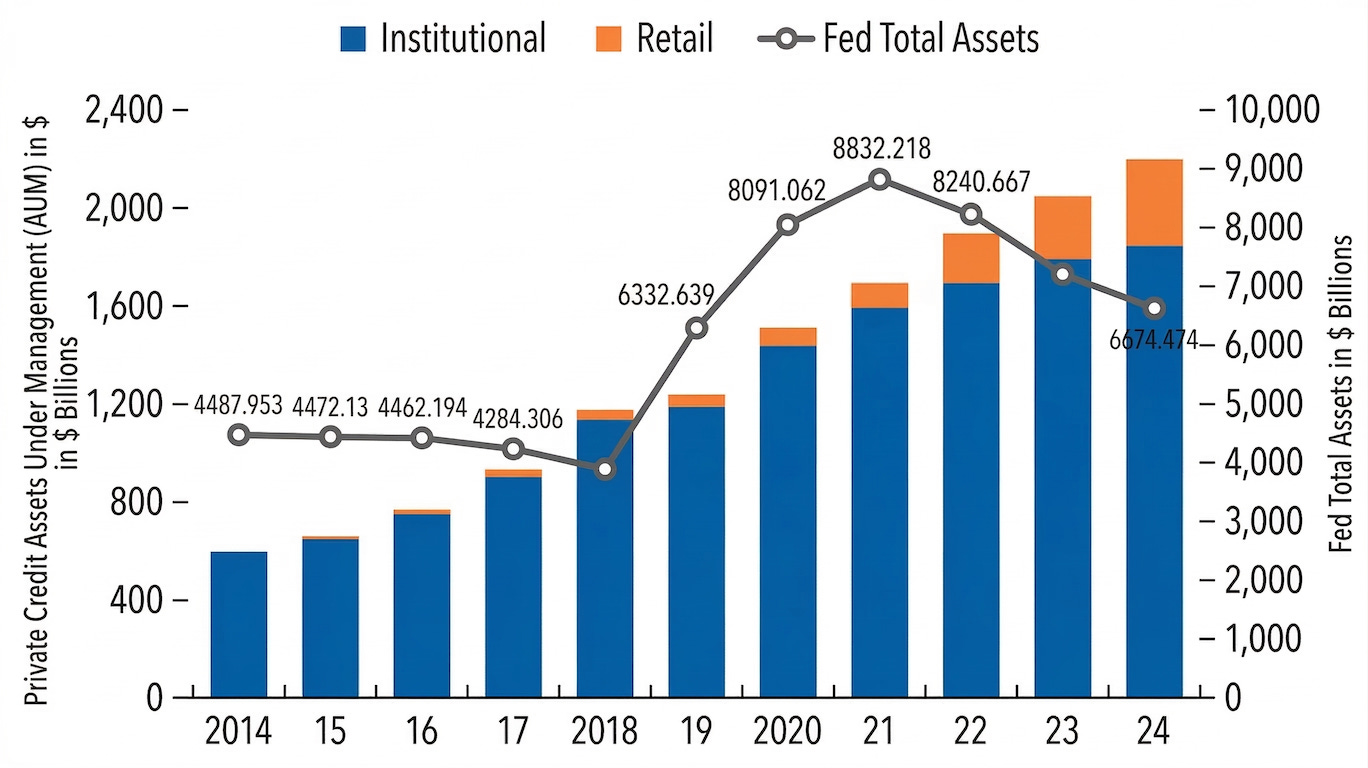

We may not have to wait much longer for the answer. The world’s largest asset managers (BlackRock, Blackstone, Blue Owl) began locking investors out of their private credit funds. Over $150 billion in retail capital now sits trapped in vehicles that cannot honor withdrawal requests. We covered in “The Big Turning” how the 2008 crisis transferred debt from private to public balance sheets. What went largely unnoticed is that by the end of the cycle, private balance sheets inflated again alongside the public ones. The ZIRP era bloated the Fed’s balance sheet to $8.9 trillion while creating an entire parallel lending system outside regulated banking, now exceeding $2 trillion. And that system is cracking.

Let’s examine how this factor is currently the top candidate to trigger The Big Turning.

What Is Private Credit?

Private credit is non-bank lending to corporations, real estate, and consumers outside the regulated banking system. It includes direct lending, Business Development Companies (BDCs), evergreen funds, and non-traded vehicles. Think of it as the shadow banking system’s latest incarnation. It’s the financial sector’s answer to the question of where do you put money when bonds yield nothing and banks face restrictions to lending.

The market grew from roughly $200 billion in 2010 to over $2 trillion in AUM by early 2026 through fund structures alone. When including the broader ecosystem of bank warehouse lines, subscription facilities, and leveraged fund-level borrowing, the total footprint approaches $3.5 trillion. This growth was a direct consequence of the ZIRP era (2008-2022) when yield-starved investors poured into private credit. This happened as banks, constrained by post-GFC regulation, retreated from riskier lending, and private credit filled the vacuum by lending to entities that the regulated system would not touch. And this has been so pervasive that the growth of private credit remained steady despite periods of Fed balance sheet contraction during The Great Stagnation.

And here’s what should sound familiar. Retail and institutional investors are marketed quarterly liquidity – typically 5% of NAV in quarterly tender offers – while the underlying assets are illiquid corporate loans with multi-year durations. Capital flows in frictionlessly but cannot be extracted during stress. This is the same maturity mismatch that destroyed Bear Stearns’ hedge funds in June 2007 and froze money market funds in September 2008. The packaging changed, but the math didn’t.

The underlying credits span five categories: large-cap corporate jumbo unitranche deals, middle-market corporate loans, commercial real estate (CRE), consumer debt (auto, student), and esoteric assets (litigation finance, IP royalties, catastrophe bonds). And all five are under stress at the same time, constituting a true systemic blowup.

The Symptoms: Redemption Lockdowns

In March 2026, BlackRock was forced to gate its $26 billion HPS Corporate Lending Fund after $1.2 billion in Q1 redemption requests, representing 9.3% of NAV. Constrained by the 5% quarterly cap, only $620 million was distributed. Nearly half of requesting investors were locked out of their own capital. Simultaneously, BlackRock wrote down a $25 million loan to Infinite Commerce Holdings from par value to zero overnight (three months earlier, the loan was marked at 100 cents on the dollar). Recall the ABX index collapse that signaled the 2007 subprime unraveling. This is its private credit cousin.

Then we have Blackstone’s $82 billion flagship fund facing record redemption requests at 7.9% of shares. To prevent a full-blown bank run, Blackstone and its executives injected $400 million of personal and corporate capital. And given the climate, management putting its own money in to stop the bleeding ended up signaling distress rather than confidence.

Blue Owl went further by halting redemptions entirely for its OBDC2 fund after demands surged to 15% of NAV. It initiated $1.4 billion in forced asset sales and shifted from quarterly tender offers to periodic distributions funded by organic liquidations. The fund in effect stopped being a fund and became a liquidating trust. Morgan Stanley and Cliffwater imposed similar restrictions, demonstrating that this sector-wide freeze is not simply a collection of isolated incidents.

The Catalysts: Why Now and Why Not Before?

This crisis is the product of a decade-long causal chain. Post-GFC ZIRP drove yield-starved capital into private credit. Cheap money fueled aggressive underwriting and the zombie company proliferation we first identified in “The Great Stagnation” (recall that over 17% of listed firms couldn’t cover interest expenses from operating income by 2017). COVID stimulus created the inflation that killed ZIRP and the Fed’s aggressive tightening from 0% to 5.5% repriced all floating-rate debt. Then while Payment-in-Kind (PIK) toggles masked the deterioration, two catalysts arrived simultaneously and the illusion shattered.

First, the Iran war. Operation Epic Fury in February 2026 sent WTI crude past $110 per barrel and threatened the Strait of Hormuz through which 20% of global LNG and 15% of crude passes. This reignited inflation at the precise moment over-leveraged borrowers needed rate cuts to survive. This froze the Fed in stagflationary paralysis while S&P estimates 100-150 basis points of additional risk premium injection. We’ve seen this movie before. Just as the 1973 Arab embargo created the stagflationary conditions that forced the Petrodollar deal (“The Great Illusion”) the 2026 energy shock recreates that trap but now with 122% debt-to-GDP instead of 35%.

Second, the “SaaS Apocalypse” is a reality as generative AI cannibalizes traditional software business models. Software companies comprise roughly 30% of BDC portfolio composition, and their per-seat subscription model is collapsing as agentic AI replaces human workers in more mundane tasks. Salesforce hit a 52-week low, down 43% year-over-year while Atlassian fell 76%, with about $2 trillion in software market cap evaporated within 30 days. The critical nuance is that even companies with growing revenue can’t refinance if their enterprise valuations drop below the collateral thresholds of their original loans. They die simply because the math of refinancing no longer works rather than effectively failing as businesses.

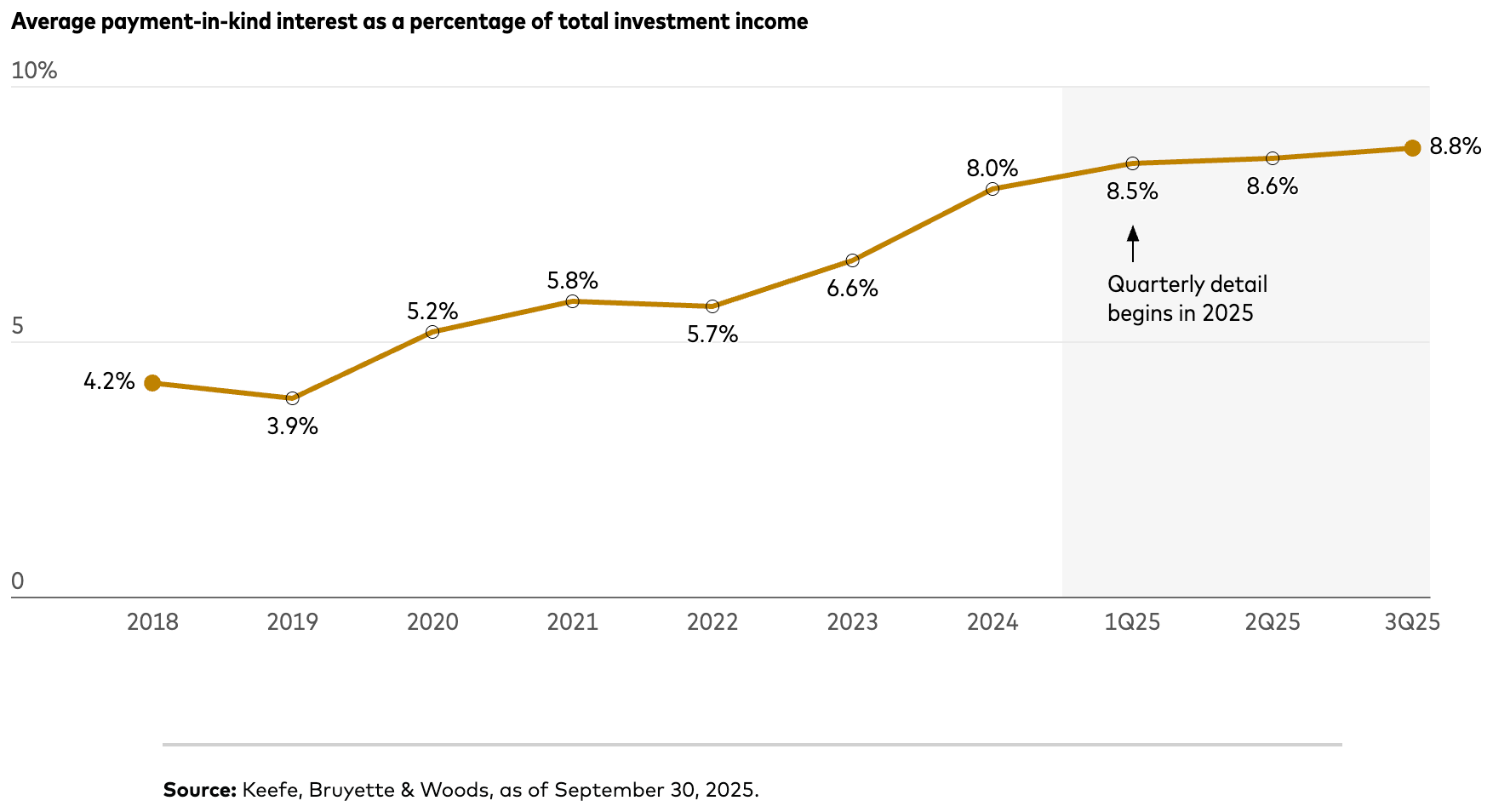

The Zombies: Payment-in-Kind and the Illusion of Stability

Payment-in-Kind (PIK) allows distressed borrowers to defer cash interest by capitalizing it onto the loan principal. The fund collects no actual cash but the loan stays marked at par on the books while the borrower survives another quarter. And the ticking time bomb of inflating principal balances grows larger with every quarter.

PIK income as a share of BDC investment income rose from 4.2% pre-pandemic to 8.8% by Q3 2025. Meanwhile, the headline private credit default rate sits at a pristine 2%. But when selective defaults, distressed exchanges, and PIK-sustained entities are properly counted, the true failure rate approaches 9%. An estimated 40% of private credit borrowers now operate with marginally extended lifespans. These are textbook zombies by the OECD definition, i.e., firms with interest coverage ratios below 1.0x for three or more consecutive years. They produce no economic value and exist solely through continuous debt rolling.

One detail worth dwelling on is that 41% of large market deals (loans exceeding $750 million) include PIK toggle features at origination as a pre-planned option. But only 7% of middle market deals have this feature natively. This means that when PIK activates in the middle market, it is almost always a reactive distress amendment, not something anyone planned for. And the middle market is where the vast majority of private credit capital is deployed.

The Maturity Wall: When All Debt Comes Due at Once

Meanwhile, multiple maturity walls are converging simultaneously. In commercial real estate, $957 billion matured in 2025, $875 billion is coming due in 2026, and $652 billion in 2027. The 2026 figure is nearly three times the 20-year historical average. In CMBS, $525 billion matures in 2026 and $587 billion in 2027. In high-yield corporate debt, $79.2 billion matures in 2026 and $140.3 billion in 2027. In the middle market, 12% of loans by count are maturing before the end of 2026.

Refinancing is impossible for most of these borrowers as SOFR rates remain elevated and the Fed cannot cut due to energy-driven inflation. Property values are depressed, with office vacancy sitting at 19.4% nationally and distress rates at 17.4% in the office sector. PIK-bloated principals are now substantially larger than the original loans, and refinancing a loan whose principal has grown 20-30% through capitalized interest at 2026 rates is a mathematical impossibility for companies with negative free cash flow.

As covered in “The Big Turning,” [1,788 banks](https://www.fau.edu/newsdesk/articles/commercial-real-estate-banking-risks-u.s.) have total CRE exposures exceeding 300% of their total capital, while 504 exceed 500%. Alternative lenders hold a disproportionate share of the near-term risk with 29% ($163 billion) of their CRE mortgages maturing in 2026. This is the moment when “extend and pretend” meets arithmetic.

The Consumer Debt Contagion

Private credit’s insatiable search for yield pushed it deep into consumer debt markets. The most spectacular casualty so far was Tricolor Holdings, a major subprime auto lender that collapsed in Chapter 7 liquidation after vehicle collateral was systematically double-pledged to multiple lenders simultaneously. JP Morgan, Barclays, and Fifth Third Bank face exposures in the half-billion-dollar range. Jamie Dimon’s infamous “cockroach” warning applies here with surgical precision: “When you see one cockroach, there’s probably more.”

The student loan market compounds the problem. Following the elimination of the Grad PLUS federal program, financing advanced education shifted to private market-based lending. This loaded private credit portfolios with uncollateralized, high-risk debt secured solely by the future earning potential of individuals entering a deteriorating labor market. As “The Big Turning” documented, AI is hollowing out precisely the white-collar entry-level positions these graduates need. Adding insult to injury, state usury laws compress margins while the political risk of federal moratoriums looms.

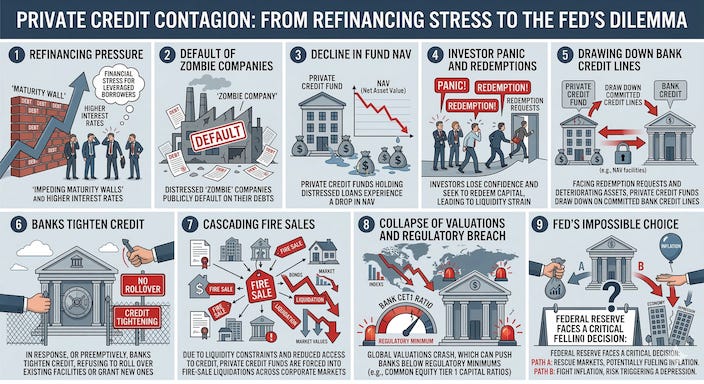

Systemic Contagion: The Shadow Banking Nexus

For a decade, the industry told itself a comforting story, that private credit “de-risked” the financial system by moving leveraged corporate loans off bank balance sheets. It was a lie. The risk didn’t leave. It was transformed, concentrated, and wired back into the banking system through complex financial plumbing.

US and European banks hold approximately $4.5 trillion in direct credit exposure to Non-Bank Financial Institutions (NBFIs), representing roughly 9% of total global loan portfolios. The 10 largest US commercial banks account for $710 billion of this exposure. Aggregate BDC borrowings from banks and non-banks reached $215 billion entering 2025, with traditional banks reporting $123 billion in committed exposures to private credit obligors.

The contagion mechanism runs in two directions. As private credit funds face redemption lockdowns and deteriorating assets, they draw down committed bank credit lines to survive, draining hundreds of billions from the traditional banking system at the moment banks need to hoard cash. Conversely, if banks defensively tighten and refuse to roll over NAV facilities, private credit funds are forced into fire-sale liquidations across corporate markets, crashing valuations globally.

European stress models show that in an adverse scenario, where private funds draw down 100% of their committed credit lines, the Common Equity Tier 1 (CET1) solvency ratios – the primary measure of a bank’s core capital buffer against losses – of 30% of the European banking sector could drop by more than a full percentage point. For context, a CET1 decline of that magnitude can push banks below regulatory minimums, triggering supervisory intervention or capital raises at the worst possible time. No comparable public stress test has been run for US banks specifically on private credit exposure, which itself is a glaring gap.

The chain of events traces a clear path. Maturity walls force refinancing at punitive rates, zombies default publicly, fund NAVs collapse, investors panic, funds drain bank credit lines, banks tighten, fire sales cascade, and the Fed faces the impossible choice: rescue markets (fueling inflation) or fight inflation (triggering depression).

The Black Box: Valuation Opacity and the Regulatory Crackdown

Private credit valuations are self-reported by fund managers with inherent conflicts of interest. The 2% headline default rate masks a 9% true failure rate. This should sound familiar. In “Winter Arrives,” we covered how the rating agencies of the 2000s operated under an issuer-pays model, rating every deal because the fees were too lucrative to refuse. Internal emails leaked during the crisis revealed the culture: “We rate every deal. It could be structured by cows, and we would rate it.”

The SEC’s current formal probes into private credit rating agencies suggest the same dynamic is playing out with inflated grades for fee-paying clients, with managers carrying toxic PIK loans at par while collecting performance fees. A former BlackRock and Bank of America employee noted publicly that private debt funds don’t carry loan loss reserves the way regulated banks must. They don’t write down non-performing loans and appear to accrue unpaid interest as if earned, no GAAP standards applied.

The Fed and the Financial Stability Oversight Council have officially recognized the systemic threat, demanding granular bank exposure reports to map contagion pathways. But here lies the paradox. SEC-mandated transparency will force write-downs. Write-downs will accelerate investor panic and redemption runs. Thus, regulation will hasten rather than prevent the reckoning.

Why This Cannot Be Stopped

Cut rates? Energy-driven inflation makes it unjustifiable. Maintain rates? 40% of private credit borrowers have negative free cash flow and can’t service their debt. It’s the 1970s stagflationary trap all over again, except the national debt was 35% of GDP then. It’s 122% now.

Fiscal stimulus is impossible, national debt stands at $37.64 trillion. Annual interest costs hit $970 billion, projected to reach $2.1 trillion by 2036. Annual deficits run at $1.9 trillion. A TARP-style bailout is politically unthinkable. The 43-day government shutdown of 2025 demonstrated that Congress cannot agree on keeping the lights on, let alone a trillion-dollar rescue. Private credit grew precisely because it was outside regulated banking. Retroactive regulation cannot unwind $2 trillion in illiquid loans already extended. The system has painted itself into a corner with no exit.

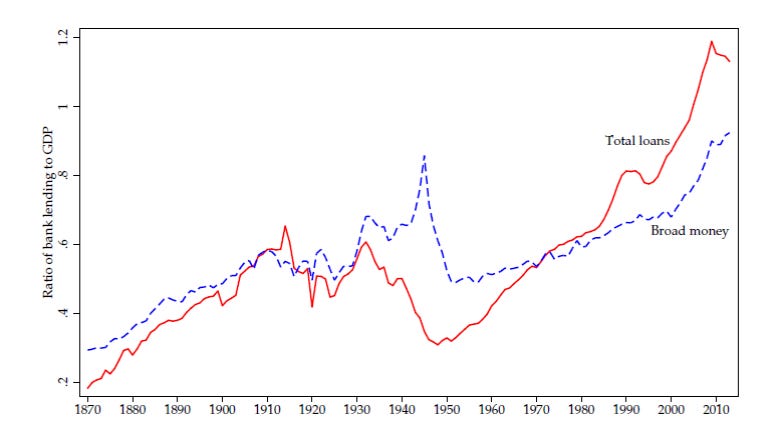

The 1930s Parallel: Shadow Banking Then and Now

In the 18 months before the 1929 crash, 30-40% of all share investments were purchased using non-bank “shadow” credit available on exchange floors, entirely outside regulated banking. Average bank credit to GDP in 1928 was about 60%, a level the US reached again around 2007. By early 2026, domestic credit to the private sector reached 200% of GDP in 2024, and over 250% when including the full financial sector. The Jorda-Schularick-Taylor Macrohistory Database produced what researchers call the “financial hockey stick.” This is the ratio of aggregate private credit to income which remained near a flat 50% plateau from 1870 until the 1970s, before surging steeply past 100%.

The structural parallels are striking. In the 1920s, trust companies served as the unregulated lending vehicles, just as BDCs and private credit funds do today. In both eras, the shadow credit grew outside regulated banking and beyond the reach of central bank monetary tools. Both periods saw asset bubbles financed by this shadow credit with equities then, corporate leveraged buyouts and CRE now. Both featured valuation opacity with minimal disclosure then, self-reported NAV today. And both were triggered by monetary tightening with margin calls in 1929, maturity walls at elevated SOFR rates in 2026.

The critical difference is what followed. In the 1930s, creative destruction was allowed to run its course, when 9,000 banks failed, unemployment hit 25%, but the economy restructured. In the 2010s, as we covered in “The Great Stagnation,” creative destruction was prevented by ZIRP, producing zombification instead of cleansing. Long-run historical data from the JST database statistically confirms that debt-financed asset bubbles outside regulated banking produce the deepest and most protracted recessions.

Ray Dalio’s Long-Term Debt Cycle and Michael Howell’s Liquidity Framework

Ray Dalio’s Big Debt Cycle framework posits that economies expand as credit grows faster than income, with short-term debt cycles building upon one another until debt burdens become unsustainable. The massive growth of private credit since 2008 represents the late stage of this cycle. This was the moment when borrowing capacity was pushed into unregulated shadow banking because the regulated system was maxed out. Zombie companies surviving on PIK are the textbook definition of Dalio’s late-cycle dynamic with borrowers who can no longer service debt with actual earnings.

Michael Howell’s Capital Wars framework adds a critical dimension. Howell estimates global debt rollovers will reach $40 trillion by 2027. His insight, which we saw in “The Great Stagnation,” is that the debt-to-liquidity ratio matters more than debt-to-GDP. Economies can sustain remarkably high debt if sufficient liquidity exists for refinancing. Japan maintains debt-to-GDP above 200% without crisis because its financial system generates adequate rollover liquidity. When that capacity dries up, the long-term debt cycle must turn. The private credit maturity wall of 2026-2027 is the specific manifestation, with $2+ trillion in shadow credit reaching the point where it can no longer be rolled over without central bank support. And this support cannot come because of inflation.

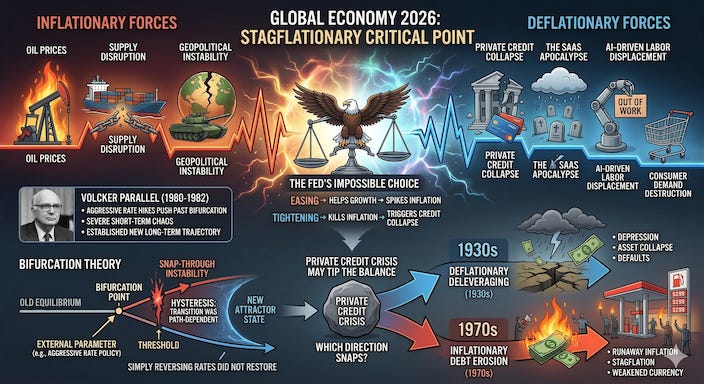

Stagflation as Phase Transition: The Physics of Opposing Forces

The stagflationary environment of 2026 resembles a thermodynamic phase transition at a critical point. Inflationary forces – oil prices, supply disruption, geopolitical instability – pull in one direction. Deflationary forces – private credit collapse, the SaaS Apocalypse, AI-driven labor displacement, consumer demand destruction – pull in the other. At the critical point, the system becomes highly unstable because the competing forces balance out without resolution. The economy cannot settle into a distinct phase, producing the wild, chaotic fluctuations that physicists call critical opalescence. The economy now faces similar circumstances: easing helps growth but spikes inflation; tightening kills inflation but triggers credit collapse.

The eventual breaking point follows what mathematicians call bifurcation theory. When an external parameter (e.g., an aggressive interest rate policy) is pushed past a specific threshold, the old equilibrium is destroyed entirely. The system experiences a snap-through instability, violently transitioning to a new attractor state. The Volcker parallel from 1980-1982 is instructive. His aggressive rate hikes pushed past the bifurcation point, creating severe short-term chaos but establishing a fundamentally new long-term trajectory. As covered in “The Great Illusion,” the economy that emerged after Volcker settled not on a return to the prior manufacturing-based order but on a new path entirely, one of financialization to the detriment of the industrial base. Because of hysteresis, the transition was path-dependent. Simply reversing rates later did not restore what had been lost.

The question for 2026 is which direction the system snaps: deflationary deleveraging (the 1930s path) or inflationary debt erosion (the 1970s path). The private credit crisis may be what tips the balance.

Synthesis: The Big Turning Is Already Here

Let’s trace what has been covered. The trillions of dollars in shadow lending, built during ZIRP to fill the vacuum left by regulated banking retreat, is cracking. BlackRock, Blackstone, and Blue Owl are gating over $150 billion in investor capital. An oil shock from the Iran war has paralyzed monetary policy while an AI disruption vaporized $2 trillion in software valuations. Underneath, 40% of borrowers have negative free cash flow, the true default rate is closer to 9% rather than 2%, and PIK accounting is the last lifeline inflating principals that must soon be refinanced. The CRE maturity wall alone is $875 billion in 2026, nearly three times the historical average. And it converges with corporate and consumer debt cliffs at the same time. Banks hold $4.5 trillion in exposure to NBFIs while every escape route is blocked. The Fed stuck in stagflation, the fiscal authority drowning in deficit, Congress incapable of action.

Private credit seems to be the final frontier of the credit expansion that defined the post-GFC era, the last place the system could push leverage when everything else was tapped out. Its unraveling connects directly to the thesis built across this series. “The Great Stagnation” showed that the post-GFC “recovery” was nominal rather than real, a hidden depression masked by QE and ZIRP. “The Big Turning” documented how all the deferred consequences arrived at once. Now the private credit reckoning reveals the potential trigger mechanism, the specific fault line where accumulated fragility converts into systemic crisis.

The 1930s Great Depression ended through WWII, which cleared accumulated malinvestment, rebooted technology, and restructured the global order at Bretton Woods. The current Great Stagnation looks like it’s approaching its own reckoning. And unlike punditry, this is not a prediction. The maturity walls are contractual obligations. The redemption lockdowns are current events. The PIK data is in public BDC filings. The banking exposure is in regulatory reports. The question is not whether it happens, but how fast and in what sequence. And whether, on the other side, the creative destruction that was deferred for fifteen years unleashes the restructuring that sets the stage for what comes next.